Small Business Loan Without Personal Guarantee: Complete 2026 Guide

Small Business Loan Without Personal Guarante: For many entrepreneurs, one of the biggest concerns when applying for financing is personal risk. This leads to a critical question: can you get a small business loan without a personal guarantee?

The short answer is yes—but it’s not easy.

A small business loan without a personal guarantee allows business owners to secure funding without putting their personal assets—such as their home, savings, or personal credit—at risk. However, because this type of loan increases risk for lenders, approval typically requires strong business financials, consistent revenue, and an established track record.

In this guide, we’ll break down how these loans work, who qualifies, and how to improve your chances of approval.

What Is a Small Business Loan Without a Personal Guarantee?

Instead, the loan is evaluated based on the business’s financial strength, credit profile, and revenue performance.

This structure is particularly attractive for business owners who want to:

Protect personal assets

Maintain financial separation between business and personal life

Operate under a limited liability structure

How Do No Personal Guarantee Business Loans Work?

Unlike traditional business loans, which often require a personal guarantee, these loans rely heavily on the business itself as the primary source of repayment.

Lenders evaluate:

Business revenue consistency

Cash flow stability

Business credit score

Time in operation

Industry risk level

Because the lender takes on more risk, these loans often come with:

Higher interest rates

Stricter qualification criteria

Lower loan amounts compared to secured loans

Many business owners work with specialized financing providers such as NF Funding, which offer flexible business funding solutions tailored to different risk profiles.

Types of Business Loans Without Personal Guarantee

While rare, several financing options may not require a personal guarantee under the right conditions.

Business Lines of Credit

Established businesses with strong financials may qualify for unsecured lines of credit based on revenue and creditworthiness.

Invoice Financing (Factoring)

Businesses can leverage unpaid invoices as collateral. The lender focuses on the customer’s ability to pay rather than the business owner.

Equipment Financing

The equipment itself acts as collateral, reducing the need for a personal guarantee.

Merchant Cash Advances

Repayment is based on daily or weekly sales, making it possible to secure funding without personal guarantees in some cases.

Corporate Credit-Based Loans

Businesses with strong corporate credit profiles may qualify without personal liability.

Who Qualifies for a Business Loan Without Personal Guarantee?

Not all businesses qualify for no personal guarantee loans. Lenders typically look for low-risk borrowers.

Common qualification criteria include:

Annual revenue of $100,000 or more

At least 1–2 years in business

Strong business credit profile

Consistent cash flow

Established customer base

These requirements help lenders reduce the risk of lending without personal backing.

Requirements for Approval

To qualify, businesses must present strong financial documentation.

Typical requirements include:

Business bank statements

Profit and loss reports

Tax returns

Business credit score

Legal business registration (LLC or corporation)

Lenders want to ensure the business can repay the loan independently.

Advantages of No Personal Guarantee Business Loans

Protects Personal Assets

Your personal property and savings are not at risk if the business cannot repay the loan.

Supports Limited Liability

These loans align with the purpose of LLCs and corporations—separating personal and business liability.

Reduces Personal Financial Risk

Business owners can scale operations without exposing personal finances.

Disadvantages and Limitations

Harder to Qualify

Lenders require strong financial performance.

Higher Interest Rates

Because of increased lender risk, costs are usually higher.

Lower Loan Amounts

Borrowing limits may be smaller compared to secured loans.

Limited Availability

Not all lenders offer no personal guarantee options.

How to Improve Your Chances of Approval

If you want to qualify for a business loan without a personal guarantee, preparation is essential.

Build Strong Business Credit

Establish credit accounts under your business name and maintain timely payments.

Increase Revenue Stability

Consistent income demonstrates your ability to repay the loan.

Separate Business and Personal Finances

Use a dedicated business bank account and financial system.

Provide Alternative Security

Assets such as equipment or receivables can strengthen your application.

Work With Specialized Lenders

Experienced lenders like NF Funding can help structure financing solutions that match your business profile.

Can Startups Get a Loan Without a Personal Guarantee?

In most cases, startups will find it very difficult to secure financing without a personal guarantee.

Because new businesses lack financial history, lenders often require:

Personal guarantees

Collateral

Co-signers

Alternative options for startups may include:

Grants

Angel investors

Venture capital

Revenue-based financing

Secured vs No Personal Guarantee Business Loans

Understanding the difference is important.

Feature

No Personal Guarantee Loan

Secured Loan

Personal liability

None

Required

Collateral

Sometimes

Required

Approval difficulty

High

Moderate

Interest rate

Higher

Lower

How to Apply for a No Personal Guarantee Business Loan

Follow these steps:

Step 1: Prepare Financial Documents

Gather all business financial records.

Step 2: Strengthen Your Credit Profile

Improve both business and personal credit scores.

Step 3: Identify Suitable Lenders

Focus on lenders that offer flexible business financing.

Step 4: Submit Application

Provide detailed business information and documentation.

Step 5: Review Loan Terms Carefully

Understand repayment structure, fees, and interest rates.

Frequently Asked Questions

Can you really get a business loan without a personal guarantee?

Yes, but it is less common and typically available only to established businesses with strong financial performance.

What credit score is needed?

Most lenders expect a strong business credit profile and may also consider personal credit scores above 650.

Are no personal guarantee loans unsecured?

Not always. Some loans may still be backed by business assets even without a personal guarantee.

Which lenders offer no personal guarantee loans?

Specialized lenders and alternative financing providers, including NF Funding, may offer flexible options depending on your business profile.

Final Thoughts: Small Business Loan Without Personal Guarantee

A small business loan without a personal guarantee can be a powerful financing option for business owners who want to protect their personal assets and operate with limited liability.

However, these loans are not easily accessible and typically require strong business performance, stable revenue, and a proven track record.

If your business meets these criteria, exploring no personal guarantee financing options can help you scale while minimizing personal financial risk. For tailored funding solutions, working with experienced providers such as NF Funding can help you identify the best financing strategy for your business.

What Is Considered a Small Business Loan? Complete Guide for 2026

What Is Considered a Small Business Loan: Access to capital is one of the most important factors in business growth. Entrepreneurs and small business owners often seek financing to support operations, expansion, or daily working requirements. However, many people are unsure about one basic question: what is considered a small business loan?

A small business loan is a financing solution designed to support businesses that operate on a relatively smaller scale in terms of revenue, workforce size, or capital requirements. These loans help companies obtain funding for working capital, equipment purchases, inventory management, or business development initiatives.

The definition of a small business loan can vary depending on the lender, industry standards, and government guidelines. Financial institutions such as NF Funding provide flexible small business financing options tailored to different business needs.

What Is Considered a Small Business Loan?

In general, a small business loan refers to financing offered to companies that require moderate capital rather than large-scale corporate funding.

Although there is no universal global standard, small business loans typically fall within the range of approximately $5,000 to $5 million, depending on the lender and business qualification criteria.

Unlike personal loans, small business loans are evaluated based on business performance metrics rather than personal spending needs. Lenders analyze factors such as business revenue stability, operational history, and repayment capability before approving funding.

How Small Business Loans Are Defined

The classification of a small business loan is influenced by both government regulations and private lending policies.

Government programs often define small businesses based on operational scale, including factors such as employee count and annual revenue. For example, many sectors consider businesses with fewer than 500 employees as small businesses, although this number can vary by industry.

Private lenders may apply more flexible criteria. Alternative financing providers, including NF Funding, may focus more on cash flow consistency and business viability rather than strict size classifications.

Typical Loan Amounts for Small Businesses

Small business loan amounts can differ significantly depending on the purpose of financing and lender policy.

Microloans generally range from a few hundred dollars to around $50,000.

Standard small business term loans often fall between $10,000 and $500,000.

Government-backed or specialized programs may offer funding up to $5 million for qualified businesses.

Smaller loans are commonly used by startups and early-stage businesses, while larger financing is typically reserved for expansion or commercial investment projects.

What Qualifies as a Small Business?

Business qualification criteria are not solely based on company size. Lenders typically evaluate multiple operational and financial indicators.

Common qualification factors include:

Number of employees

Annual business revenue

Industry classification

Business credit history

Length of business operation

Some financing providers place greater emphasis on revenue performance and repayment capacity rather than strict organizational size.

Types of Small Business Loans

Term Loans

Traditional term loans provide a fixed amount of capital that is repaid over a predetermined schedule. These loans are often used for equipment purchases, expansion projects, and operational investments.

SBA-Style Loans

Government-backed financing programs are designed to reduce lending risk and support small business growth. These loans often offer competitive interest rates and longer repayment periods.

Business Line of Credit

A business line of credit functions similarly to a credit card, allowing businesses to withdraw funds when needed and pay interest only on the amount used.

Equipment Financing

Equipment financing allows businesses to purchase machinery or technology by using the purchased equipment as collateral.

Revenue-Based Financing

Some modern lenders offer financing solutions where repayment is linked to business revenue performance.

Businesses exploring flexible funding opportunities may consider providers such as NF Funding.

What Can Small Business Loans Be Used For?

Small business financing can support various operational and growth activities, including:

Working capital management

Inventory procurement

Marketing and business development

Hiring and workforce expansion

Technology and equipment investment

Office or facility improvement

Proper utilization of business loans can help improve productivity and long-term profitability.

Requirements for Obtaining a Small Business Loan

Lenders evaluate several financial and operational factors before approving business financing.

Typical requirements may include:

Business financial statements

Credit history and credit score evaluation

Revenue documentation

Business operational history

Collateral for secured financing

Alternative financing providers such as NF Funding may offer more flexible eligibility criteria compared to traditional banking institutions.

Secured vs Unsecured Small Business Loans

Small business loans can be categorized into secured and unsecured financing.

Secured loans require collateral such as commercial property, equipment, or business assets. These loans generally offer lower interest rates and higher borrowing limits.

Unsecured loans do not require collateral but may involve higher interest rates and stricter credit evaluation.

How to Apply for a Small Business Loan

The application process typically involves several stages:

Assess your funding requirements

Select the appropriate loan type

Prepare financial and business documents

Compare multiple lenders

Submit the loan application

Working with experienced financing providers such as NF Funding can help streamline the approval process.

Advantages of Small Business Loans

Small business loans provide essential financial flexibility for entrepreneurs.

Key benefits include:

Access to immediate working capital

Opportunity for business expansion

Improved cash flow management

Equipment and infrastructure investment support

Frequently Asked Questions

What is considered a small business loan?

A small business loan is financing designed for companies requiring moderate capital, typically ranging from approximately $5,000 to several million dollars depending on the lender.

Who qualifies for a small business loan?

Qualification depends on business revenue, credit history, operational stability, and repayment capacity.

Can startups obtain small business loans?

Yes, some lenders offer startup financing, although requirements may include business planning, strong credit performance, or collateral.

What interest rate applies to small business loans?

Interest rates vary depending on loan type, lender policy, and borrower risk profile.

How fast can small business loans be approved?

Some alternative lenders can approve loans within a few days, while traditional banking institutions may require several weeks.

Final Thoughts: What Is Considered a Small Business Loan? Complete Guide for 2026

Small business loans play a vital role in supporting entrepreneurial growth and economic development. Understanding what is considered a small business loan helps business owners select appropriate financing options based on their operational requirements.

Whether you need working capital, equipment financing, or expansion funding, choosing the right lender is essential for sustainable business success. Financial institutions such asNF Funding provide flexible financing solutions designed to help small businesses achieve their growth goals.

Small Business Acquisition Loans: How to Finance Buying a Business

Small Business Acquisition Loans: Buying an existing business can be one of the fastest and most strategic ways to become an entrepreneur. Instead of starting from scratch, you gain access to an established customer base, proven operations, and immediate cash flow. However, most buyers do not have enough capital upfront—which is where small business acquisition loans come into play.

These loans are specifically designed to help individuals and investors finance the purchase of an existing business. Whether you are acquiring a local company or expanding your portfolio, structured financing options—such as those offered by NF Funding—can make business ownership more accessible.

In this guide, we’ll break down how acquisition loans work, the types available, qualification requirements, and how to secure funding successfully.

What Are Small Business Acquisition Loans?

A small business acquisition loan is a type of financing used to purchase an existing business or ownership stake.

These loans can cover:

Business purchase price

Equipment and inventory

Operational costs after acquisition

Refinancing of existing business debt

Lenders evaluate both the buyer and the target business, focusing on financial performance, stability, and future earning potential.

How Do Business Acquisition Loans Work?

Unlike traditional loans, acquisition financing involves analyzing two key elements:

1. The Buyer

Lenders assess your:

Credit score

Financial background

Industry experience

Management capability

2. The Business Being Acquired

Lenders review:

Revenue and profitability

Cash flow stability

Customer base

Market position

The loan is typically repaid using the cash flow generated by the acquired business, making its financial health critical to approval.

Types of Small Business Acquisition Loans

SBA 7(a) Acquisition Loans

SBA-backed loans are among the most popular options.

Key features:

Loan amounts up to $5 million

Lower down payment requirements

Competitive interest rates

Longer repayment terms

Traditional Bank Loans

Banks offer acquisition financing with:

Lower interest rates

Strict approval criteria

Strong documentation requirements

These loans are ideal for borrowers with excellent credit and experience.

Seller Financing

In some cases, the current owner finances part of the purchase.

Benefits include:

Faster approval

Flexible repayment terms

Lower upfront capital requirement

Alternative / Private Lenders

Alternative lenders provide:

Faster approvals

Flexible qualification criteria

Shorter funding timelines

Many buyers explore options through providers such as NF Funding for more flexible financing solutions.

What Can Acquisition Loans Be Used For?

Acquisition loans are versatile and can be used for:

Purchasing an existing business

Buying shares or ownership stakes

Acquiring inventory and equipment

Covering initial operating expenses

Refinancing existing business obligations

Requirements for Small Business Acquisition Loans

To qualify, borrowers typically need to meet specific financial and professional criteria.

Credit Score

Most lenders require a credit score of 650 or higher.

Down Payment

Buyers usually need to invest 10% to 30% of the purchase price.

Business Financials

You’ll need access to:

Profit and loss statements

Tax returns

Cash flow reports

Industry Experience

Relevant experience increases lender confidence in your ability to manage the business.

Strong Cash Flow

The target business must demonstrate the ability to repay the loan.

How Much Can You Borrow?

Loan amounts vary depending on the lender and deal size.

Loan Type

Typical Amount

SBA Loans

Up to $5 million

Bank Loans

$100,000 – $3 million

Alternative Lenders

$50,000 – $1 million

Down Payment Requirements

Down payments are a critical part of acquisition financing.

Typical structure:

Buyer contribution: 10%–20%

Seller financing: 5%–10%

Lender financing: remaining amount

Combining these sources can make deals more achievable.

Pros and Cons of Small Business Acquisition Loans

Advantages

Faster entry into business ownership

Immediate revenue generation

Lower risk compared to startups

Established customer base

Disadvantages

Requires upfront capital

Ongoing debt repayment

Complex due diligence process

Risk of overpaying for the business

How to Qualify for a Business Acquisition Loan

Improving your chances of approval requires preparation.

Prepare Financial Documents

Ensure all financial records are accurate and complete.

Evaluate the Business Carefully

Conduct detailed due diligence before applying.

Build a Strong Credit Profile

Maintain a good credit score and financial history.

Demonstrate Industry Knowledge

Show lenders that you understand the business and market.

Step-by-Step: How to Get a Business Acquisition Loan

Step 1: Identify a Business to Acquire

Choose a business with strong financial performance.

Step 2: Conduct Due Diligence

Analyze financial records, operations, and risks.

Step 3: Determine Financing Needs

Calculate total acquisition cost and funding gap.

Step 4: Choose the Right Lender

Compare banks, SBA lenders, and alternative financing providers.

Step 5: Submit Loan Application

Provide financial documents and business details.

Step 6: Close the Deal

Finalize agreements and complete the acquisition.

Working with experienced lenders such as NF Funding can streamline this process.

Seller Financing vs Bank Loans

Feature

Seller Financing

Bank Loan

Approval speed

Faster

Slower

Flexibility

High

Low

Documentation

Minimal

Extensive

Risk

Shared

Mostly buyer

Risks of Business Acquisition Financing

While acquisition loans provide opportunity, they also involve risk.

Overvaluation Risk

Paying too much for a business can reduce profitability.

Financial Misrepresentation

Inaccurate financial records can mislead buyers.

Market Changes

Economic conditions may impact business performance.

Operational Challenges

Managing a new business comes with learning curves.

Frequently Asked Questions

Can you get a loan to buy a small business?

Yes, many lenders offer acquisition loans specifically designed to finance business purchases.

What credit score is needed?

Most lenders require a credit score of at least 650, although higher scores improve approval chances.

Do banks finance business acquisitions?

Yes, traditional banks and SBA lenders commonly provide acquisition financing.

How long does approval take?

Approval timelines range from a few days (alternative lenders) to several weeks (banks).

Final Thoughts: Small Business Acquisition Loans

Small business acquisition loans provide a powerful pathway to business ownership without starting from zero. With the right financing structure, buyers can acquire profitable businesses and begin generating income immediately.

However, success depends on careful planning, strong financial evaluation, and choosing the right funding partner. Whether you are purchasing your first business or expanding your portfolio, working with experienced lenders such as NF Funding can help you navigate the process and secure the right financing solution.

What Is Considered a Small Business Loan? Complete Guide for 2026

Access to capital is one of the most important factors in business growth. Entrepreneurs and small business owners often seek financing to support operations, expansion, or daily working requirements. However, many people are unsure about one basic question: what is considered a small business loan?

A small business loan is a financing solution designed to support businesses that operate on a relatively smaller scale in terms of revenue, workforce size, or capital requirements. These loans help companies obtain funding for working capital, equipment purchases, inventory management, or business development initiatives.

The definition of a small business loan can vary depending on the lender, industry standards, and government guidelines. Financial institutions such as NF Funding provide flexible small business financing options tailored to different business needs.

What Is Considered a Small Business Loan?

In general, a small business loan refers to financing offered to companies that require moderate capital rather than large-scale corporate funding.

Although there is no universal global standard, small business loans typically fall within the range of approximately $5,000 to $5 million, depending on the lender and business qualification criteria.

Unlike personal loans, small business loans are evaluated based on business performance metrics rather than personal spending needs. Lenders analyze factors such as business revenue stability, operational history, and repayment capability before approving funding.

How Small Business Loans Are Defined

The classification of a small business loan is influenced by both government regulations and private lending policies.

Government programs often define small businesses based on operational scale, including factors such as employee count and annual revenue. For example, many sectors consider businesses with fewer than 500 employees as small businesses, although this number can vary by industry.

Private lenders may apply more flexible criteria. Alternative financing providers, including NF Funding, may focus more on cash flow consistency and business viability rather than strict size classifications.

Typical Loan Amounts for Small Businesses

Small business loan amounts can differ significantly depending on the purpose of financing and lender policy.

Microloans generally range from a few hundred dollars to around $50,000.

Standard small business term loans often fall between $10,000 and $500,000.

Government-backed or specialized programs may offer funding up to $5 million for qualified businesses.

Smaller loans are commonly used by startups and early-stage businesses, while larger financing is typically reserved for expansion or commercial investment projects.

What Qualifies as a Small Business?

Business qualification criteria are not solely based on company size. Lenders typically evaluate multiple operational and financial indicators.

Common qualification factors include:

Number of employees

Annual business revenue

Industry classification

Business credit history

Length of business operation

Some financing providers place greater emphasis on revenue performance and repayment capacity rather than strict organizational size.

Types of Small Business Loans

Term Loans

Traditional term loans provide a fixed amount of capital that is repaid over a predetermined schedule. These loans are often used for equipment purchases, expansion projects, and operational investments.

SBA-Style Loans

Government-backed financing programs are designed to reduce lending risk and support small business growth. These loans often offer competitive interest rates and longer repayment periods.

Business Line of Credit

A business line of credit functions similarly to a credit card, allowing businesses to withdraw funds when needed and pay interest only on the amount used.

Equipment Financing

Equipment financing allows businesses to purchase machinery or technology by using the purchased equipment as collateral.

Revenue-Based Financing

Some modern lenders offer financing solutions where repayment is linked to business revenue performance.

Businesses exploring flexible funding opportunities may consider providers such as NF Funding.

What Can Small Business Loans Be Used For?

Small business financing can support various operational and growth activities, including:

Working capital management

Inventory procurement

Marketing and business development

Hiring and workforce expansion

Technology and equipment investment

Office or facility improvement

Proper utilization of business loans can help improve productivity and long-term profitability.

Requirements for Obtaining a Small Business Loan

Lenders evaluate several financial and operational factors before approving business financing.

Typical requirements may include:

Business financial statements

Credit history and credit score evaluation

Revenue documentation

Business operational history

Collateral for secured financing

Alternative financing providers such as NF Funding may offer more flexible eligibility criteria compared to traditional banking institutions.

Secured vs Unsecured Small Business Loans

Small business loans can be categorized into secured and unsecured financing.

Secured loans require collateral such as commercial property, equipment, or business assets. These loans generally offer lower interest rates and higher borrowing limits.

Unsecured loans do not require collateral but may involve higher interest rates and stricter credit evaluation.

How to Apply for a Small Business Loan

The application process typically involves several stages:

Assess your funding requirements

Select the appropriate loan type

Prepare financial and business documents

Compare multiple lenders

Submit the loan application

Working with experienced financing providers such as NF Funding can help streamline the approval process.

Advantages of Small Business Loans

Small business loans provide essential financial flexibility for entrepreneurs.

Key benefits include:

Access to immediate working capital

Opportunity for business expansion

Improved cash flow management

Equipment and infrastructure investment support

Frequently Asked Questions

What is considered a small business loan?

A small business loan is financing designed for companies requiring moderate capital, typically ranging from approximately $5,000 to several million dollars depending on the lender.

Who qualifies for a small business loan?

Qualification depends on business revenue, credit history, operational stability, and repayment capacity.

Can startups obtain small business loans?

Yes, some lenders offer startup financing, although requirements may include business planning, strong credit performance, or collateral.

What interest rate applies to small business loans?

Interest rates vary depending on loan type, lender policy, and borrower risk profile.

How fast can small business loans be approved?

Some alternative lenders can approve loans within a few days, while traditional banking institutions may require several weeks.

Final Thoughts

Small business loans play a vital role in supporting entrepreneurial growth and economic development. Understanding what is considered a small business loan helps business owners select appropriate financing options based on their operational requirements.

Whether you need working capital, equipment financing, or expansion funding, choosing the right lender is essential for sustainable business success. Financial institutions such as NF Funding provide flexible financing solutions designed to help small businesses achieve their growth goals.

Is a Small Business Loan Secured or Unsecured? Key Differences Explained (2026 Guide)

When business owners begin searching for funding, one of the most common questions they ask is: is a small business loan secured or unsecured?

The answer is that small business loans can be either secured or unsecured, depending on the lender, loan amount, and the borrower’s financial profile. Some loans require collateral such as property or equipment, while others are approved based on your creditworthiness and business revenue.

Understanding the difference between secured and unsecured business loans is essential because it affects interest rates, loan limits, approval speed, and financial risk. In this guide, we’ll explain how both types of loans work and help you determine which option may be best for your business.

Many entrepreneurs also explore flexible funding options through lenders such as NF Funding, which provide different financing solutions tailored to small businesses.

Is a Small Business Loan Secured or Unsecured?

A small business loan can be secured or unsecured, depending on whether the lender requires collateral.

A secured business loan requires the borrower to pledge assets—such as property, equipment, or inventory—as collateral for the loan. If the borrower fails to repay the loan, the lender may claim the collateral.

An unsecured business loan, on the other hand, does not require physical collateral. Instead, lenders evaluate factors such as credit score, business revenue, and financial history to determine eligibility.

What Is a Secured Small Business Loan?

A secured small business loan is a loan backed by collateral that the lender can claim if the borrower fails to repay the debt.

Collateral reduces the lender’s risk, which is why secured loans often offer larger loan amounts and lower interest rates compared to unsecured loans.

Common types of collateral include:

Commercial real estate

Business equipment

Inventory

Vehicles

Accounts receivable

Personal assets in some cases

Because lenders have a financial safety net, they are usually more willing to approve larger funding amounts for secured loans.

What Is an Unsecured Small Business Loan?

An unsecured small business loan does not require the borrower to pledge collateral.

Instead, lenders evaluate the borrower based on financial strength, including:

Credit score

Business revenue

Length of time in business

Cash flow stability

Because unsecured loans carry more risk for lenders, they usually come with:

higher interest rates

lower borrowing limits

shorter repayment terms

However, many businesses prefer unsecured loans because they do not risk losing valuable assets.

Key Differences Between Secured and Unsecured Business Loans

Understanding the differences between these two types of loans can help you choose the right financing option.

Feature

Secured Business Loan

Unsecured Business Loan

Collateral

Required

Not required

Interest rates

Lower

Higher

Loan amount

Higher

Lower

Approval speed

Slower

Faster

Risk to borrower

Asset risk

No asset risk

The best option depends on your business’s financial situation and how quickly you need funding.

When Should You Choose a Secured Business Loan?

A secured loan may be the better choice if your business needs larger amounts of capital or long-term financing.

Situations where secured loans are often used include:

Business Expansion

Companies expanding operations may need significant funding to open new locations or hire additional staff.

Equipment Purchases

Businesses purchasing expensive equipment often secure loans using the equipment itself as collateral.

Commercial Property Purchases

Secured loans are commonly used for commercial real estate investments.

Lower Interest Rate Goals

Businesses seeking lower borrowing costs often choose secured financing.

When Should You Choose an Unsecured Business Loan?

Unsecured loans can be ideal for businesses that need quick access to smaller amounts of funding.

Common situations include:

Short-Term Cash Flow Needs

Businesses experiencing temporary cash flow gaps may prefer unsecured financing.

Fast Funding Requirements

Unsecured loans usually have faster approval processes than secured loans.

Businesses Without Collateral

Startups or service-based businesses may not have physical assets to pledge as collateral.

Types of Secured Small Business Loans

Several types of secured loans are available to businesses depending on their financing needs.

Equipment Financing

Businesses can use equipment itself as collateral for loans used to purchase machinery or tools.

Commercial Real Estate Loans

These loans are secured by commercial property used for business operations or investment purposes.

Inventory Financing

Retailers and wholesalers may use inventory as collateral for working capital loans.

Invoice Financing

Businesses can use outstanding invoices as collateral to receive immediate funding.

Types of Unsecured Small Business Loans

Unsecured financing options are popular among small businesses seeking flexible funding.

Business Lines of Credit

A revolving credit line that businesses can draw from when needed.

Merchant Cash Advances

Funding based on future credit card sales.

Short-Term Business Loans

These loans provide fast capital with repayment periods typically under two years.

Revenue-Based Financing

Repayments are based on a percentage of business revenue.

Many business owners explore these options through lenders such as NF Funding, which offer flexible financing solutions.

Which Small Business Loan Is Easier to Get?

Whether a secured or unsecured loan is easier to obtain depends on the borrower’s financial profile.

Secured loans may be easier to qualify for if:

you have valuable collateral

your credit score is lower

you need a large loan amount

Unsecured loans may be easier if:

you have strong credit

your business generates stable revenue

you need smaller funding quickly

Lenders evaluate multiple factors before approving business financing.

Pros and Cons of Secured Business Loans

Advantages

Lower interest rates

Higher borrowing limits

Longer repayment terms

Disadvantages

Risk of losing collateral

Longer approval process

Additional documentation required

Pros and Cons of Unsecured Business Loans

Advantages

No collateral required

Faster approval times

Easier application process

Disadvantages

Higher interest rates

Smaller loan amounts

Shorter repayment terms

How to Qualify for a Small Business Loan

Lenders typically evaluate several key factors before approving a business loan.

Common requirements include:

Business financial statements

Credit score and credit history

Revenue documentation

Time in business

Business plan or funding purpose

Preparing these documents in advance can improve your chances of approval.

How to Apply for a Small Business Loan

Applying for a business loan generally involves several steps.

Step 1: Determine Your Financing Needs

Decide how much funding your business requires and how it will be used.

Step 2: Choose the Right Loan Type

Select between secured or unsecured financing based on your business situation.

Step 3: Gather Financial Documents

Prepare bank statements, tax returns, and financial records.

Step 4: Compare Lenders

Research lenders offering competitive loan terms.

Step 5: Submit Your Application

Complete the loan application and provide supporting documentation.

Businesses seeking flexible funding solutions often consider lenders such as NF Funding for their financing needs.

Frequently Asked Questions

Are most small business loans secured?

Many traditional bank loans are secured, especially for large loan amounts. However, many alternative lenders offer unsecured business loans for smaller funding needs.

Can you get a business loan without collateral?

Yes. Many lenders offer unsecured business loans that do not require collateral, although they may have higher interest rates and stricter credit requirements.

What credit score is needed for an unsecured business loan?

Most lenders require a credit score of around 650 or higher, although requirements may vary depending on the lender and loan type.

What assets can be used as collateral for a business loan?

Common forms of collateral include commercial property, equipment, inventory, vehicles, and accounts receivable.

Final Thoughts

So, is a small business loan secured or unsecured?

The answer is that both options exist, and the best choice depends on your business’s financial situation, funding needs, and risk tolerance.

Secured loans generally offer larger funding amounts and lower interest rates, while unsecured loans provide faster approvals and eliminate the need for collateral.

By understanding the differences between these financing options, business owners can choose the loan structure that best supports their growth strategy.

For businesses exploring flexible financing options, experienced lenders such as NF Funding provide funding solutions designed to support small business growth and expansion.

Introduction & Overview of Business Loans for Small Businesses

Business Loans for Small Businesses: Running a small business often requires external financing to fund growth, cover operational expenses, or manage unexpected costs. Business loans for small businesses are a critical tool that allows owners to access capital without diluting ownership or waiting for revenue to accumulate. They provide the liquidity necessary to seize opportunities, expand operations, hire staff, or invest in technology and equipment.

Small business loans differ significantly from personal loans. Lenders assess the business’s ability to generate revenue, repay the loan, and manage cash flow effectively. Unlike venture capital, loans do not require giving up equity, which makes them attractive to founders who want to retain full control.

In 2026, small businesses have access to an unprecedented variety of lending options, ranging from traditional bank loans to online lenders and government-backed programs such as SBA loans. Each type of loan serves a distinct purpose, carries different costs, and requires varying qualifications. Understanding the nuances of each option allows business owners to make informed financing decisions, optimize their capital structure, and minimize financial risk.

This comprehensive guide aims to provide small business owners, entrepreneurs, and financial decision-makers with a complete roadmap for navigating the complex world of business financing. It covers the mechanics of small business loans, eligibility requirements, interest rates, repayment structures, and real-world case studies. Additionally, this guide addresses geographic considerations for local lenders, outlines best practices for lender selection, and explains how to match funding options with business goals.

By the end of this article, readers will gain actionable insights into how to evaluate, secure, and use business loans to grow their small business sustainably while avoiding common pitfalls. This article is written in international English and optimized to rank in Google, targeting both informational and commercial intent queries.

What Are Business Loans for Small Businesses?

Business loans for small businesses are short-term or long-term financing options specifically designed to meet the unique needs of small business operations. These loans can be used to fund a variety of purposes including working capital, equipment purchases, inventory acquisition, marketing campaigns, and expansion projects. Unlike personal loans, these loans are evaluated primarily based on the business’s ability to generate revenue and repay the debt, often with a secondary focus on the owner’s personal credit profile.

Small business loans can be structured in different ways:

Term loans provide a lump sum upfront, repaid over a fixed period at either a fixed or variable interest rate.

Lines of credit allow businesses to borrow as needed up to a certain limit, offering flexibility to manage cash flow fluctuations.

Asset-based loans are secured by business assets such as equipment or receivables.

Government-backed loans, such as SBA loans in the United States, offer lower rates and longer terms for eligible businesses.

The primary advantage of small business loans is that they provide predictable, structured capital without requiring business owners to give up equity or control. They allow entrepreneurs to leverage borrowed funds to achieve growth objectives and generate revenue that exceeds the cost of borrowing.

For lenders, small business loans are assessed on three main criteria:

Creditworthiness of the business

Revenue and cash flow stability

Business plan and repayment strategy

By understanding the mechanics of these loans, business owners can make informed decisions that balance financial risk with growth opportunities.

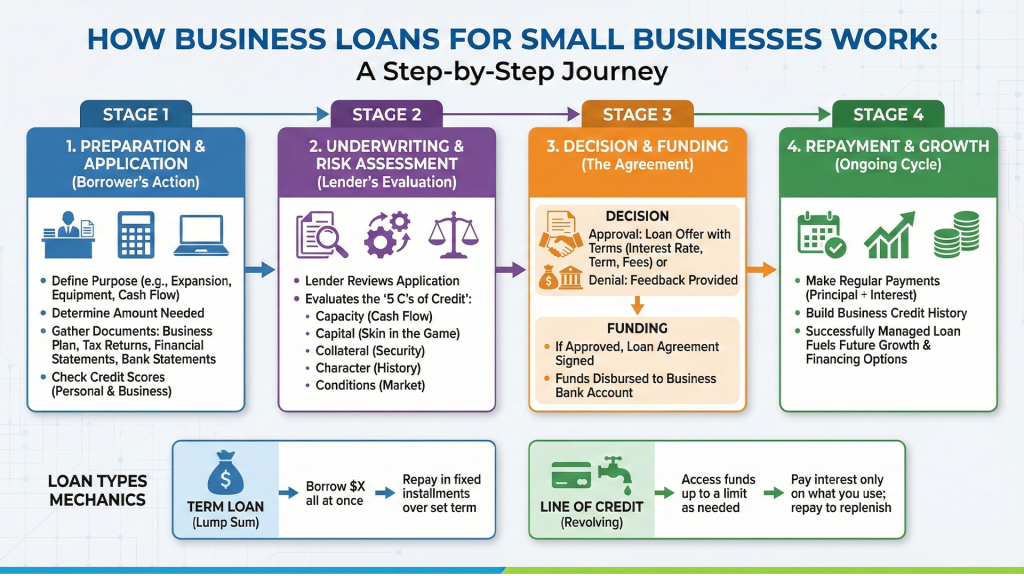

How Business Loans for Small Businesses Work

Small business loans function as agreements between the lender and the borrower, where the lender provides a specified amount of capital and the borrower agrees to repay it over a defined period with interest. The process generally involves several steps:

Identifying Funding Needs

Before applying, business owners must define the purpose and scope of the financing. This could include expanding operations, purchasing inventory, hiring staff, upgrading technology, or bridging cash flow gaps. Clearly identifying funding needs allows the borrower to select the most suitable type of loan and avoid overborrowing.

Choosing the Right Loan Type

Each business loan type has unique characteristics. Term loans provide upfront capital for significant investments but require regular fixed payments. Lines of credit are flexible and best suited for recurring or unpredictable expenses. SBA loans, while slower to approve, offer favorable interest rates and extended terms for eligible small businesses. Asset-based loans use business assets as collateral, reducing risk for lenders while providing access to higher capital amounts.

Application and Approval Process

The application typically requires documentation such as financial statements, tax returns, bank statements, business plans, and details about existing debt. Lenders assess the business’s creditworthiness, revenue consistency, and repayment capacity. Approval timelines can vary: traditional banks may take several weeks, whereas online lenders often approve loans within days.

Loan Disbursement and Repayment Structure

Once approved, funds are disbursed according to the loan agreement. Term loans usually provide a lump sum, whereas lines of credit allow incremental withdrawals. Repayment can be structured as fixed monthly payments, interest-only payments, or a combination of both. Understanding repayment obligations is crucial for maintaining cash flow and avoiding default.

Types of Business Loans for Small Businesses

Choosing the right type of business loan is critical to ensuring that your funding aligns with both short-term needs and long-term business goals. Different loans are structured to serve distinct purposes, and understanding the nuances of each can save you from high costs, unnecessary risk, and funding delays. This section explores the most popular and effective business loan types for small businesses in 2026.

Term Loans for Small Businesses

Term loans are one of the most traditional and widely used forms of business financing. They involve borrowing a fixed amount of money upfront and repaying it over a predetermined period with interest. Term loans can be short-term (generally under one year) or long-term (up to 10 years or more) depending on the lender and purpose.

Short-term loans are often used for immediate working capital, seasonal inventory needs, or urgent equipment purchases. Long-term loans are better suited for major investments such as property acquisition, business expansion, or technology upgrades.

Key characteristics of term loans include:

Fixed or variable interest rates

Structured repayment schedules (monthly, quarterly, or semi-annual)

The advantage of term loans lies in their simplicity and predictability. Businesses know exactly how much they owe and when repayment is due. However, term loans may require collateral, a strong credit profile, and evidence of consistent revenue to secure favorable rates.

Businesses that choose term loans benefit from stable financing costs, making it easier to forecast expenses. However, misalignment between loan term and project timeline can increase the effective cost if repayments start before revenue from the financed project materializes.

SBA Loans for Small Businesses

Small Business Administration (SBA) loans are government-backed loans that provide favorable terms for eligible small businesses. SBA loans are popular because they combine relatively low interest rates with longer repayment terms, making them more manageable than traditional bank loans.

Common SBA loan programs include:

SBA 7(a) loans: Flexible financing for working capital, equipment, or expansion

SBA 504 loans: Long-term, fixed-rate financing for major fixed assets like real estate

SBA Microloans: Smaller loans for startups or businesses with limited credit history

SBA loans are highly structured, often requiring detailed business plans, financial statements, and extensive documentation. Approval timelines are longer than other loan types, ranging from several weeks to a few months. Despite this, the benefits—lower interest rates, longer terms, and partial government guarantees—make SBA loans a preferred option for many small business owners.

SBA loans are particularly suitable for startups and small businesses that need sizable capital but do not want to pay high interest rates or provide large cash reserves upfront. These loans also build credibility for the business, often easing future access to financing.

Business Lines of Credit

A business line of credit is a flexible financing solution that allows businesses to borrow funds up to a pre-approved limit. Unlike term loans, lines of credit work like a revolving credit account. Borrowers can withdraw, repay, and redraw as needed, which makes it ideal for managing cash flow fluctuations, seasonal expenses, or short-term funding gaps.

Key features include:

Interest is charged only on the amount drawn

Flexible repayment options

Typically renewable annually

Lines of credit are particularly useful for businesses with variable revenue streams or unexpected expenses. They provide liquidity without the commitment of a fixed-term loan, allowing businesses to respond quickly to opportunities or emergencies.

The primary consideration is that interest rates may be variable, and some lenders require regular financial reporting. Responsible usage ensures that a line of credit supports growth rather than creating cyclical debt problems.

Equipment Financing Loans

Equipment financing loans are specialized loans designed to help businesses purchase or lease equipment without depleting cash reserves. The purchased equipment typically serves as collateral, reducing the lender’s risk and sometimes allowing higher borrowing amounts or better terms.

Advantages of equipment financing include:

Preserves working capital

Spreads the cost of equipment over time

Often tax-deductible

These loans are ideal for businesses requiring machinery, vehicles, or technology essential to operations. Repayment terms vary based on equipment lifespan and depreciation schedules. Like other asset-based financing, approval can be faster because collateral reduces lender risk.

Invoice Financing and Factoring

Invoice financing or factoring allows businesses to access cash tied up in unpaid invoices. The lender advances a percentage of the invoice value, providing immediate liquidity while the lender collects payment from clients.

This method is particularly helpful for businesses with long payment cycles or B2B operations where clients may take 30–90 days to pay.

Key considerations:

Fees or interest charged on the advanced amount

Speeds up cash flow

Does not increase long-term debt

Invoice financing helps maintain operations without waiting for customer payments and is ideal for businesses experiencing rapid growth or temporary cash flow crunches.

Merchant Cash Advances

A merchant cash advance (MCA) provides a lump sum upfront, repaid through a percentage of daily credit/debit card sales. While approval is fast and documentation minimal, MCAs come with high effective interest rates and can strain cash flow if sales decline.

Pros:

Quick funding (often within days)

No collateral required

Flexible repayments linked to revenue

Cons:

Extremely high cost compared to other loans

Potential for cash flow issues

MCAs are generally recommended only for short-term emergency funding or businesses with strong, consistent daily sales.

Requirements, Rates, ROI, and Real-World Case Study

Accessing business loans for small businesses requires more than just an application. Lenders assess the business’s financial health, creditworthiness, and repayment capability to minimize risk. Understanding these requirements and the true cost of borrowing ensures you choose the right loan, manage repayments effectively, and maximize growth.

Requirements for Small Business Loans

Lenders have specific requirements, which vary depending on the type of loan and the lender’s risk appetite. However, several criteria are consistently evaluated across all small business financing options.

Credit Score A strong credit score—both personal and business—is often required. Banks typically prefer scores above 650, while alternative lenders may accept lower scores if other factors, like revenue and collateral, are strong. Your credit score influences interest rates, loan amounts, and approval speed.

Business Revenue and Cash Flow Lenders want assurance that your business generates enough revenue to repay the loan. Monthly or annual revenue, profit margins, and cash flow statements are critical. Businesses with irregular income streams may need to demonstrate historical performance or provide guarantees.

Time in Business Many lenders prefer businesses that have operated for at least 1–2 years. Startups may qualify for SBA microloans, lines of credit, or private lending, but terms may be more conservative.

Collateral and Personal Guarantees Collateral reduces lender risk. This may include equipment, inventory, accounts receivable, or real estate. Some loans require a personal guarantee from the owner, making them personally liable if the business defaults.

Documentation Required documentation includes financial statements, tax returns, business plans, bank statements, and existing debt details. SBA loans are particularly documentation-intensive, requiring detailed business plans and forecasts.

Meeting these requirements increases the likelihood of approval, lowers borrowing costs, and ensures the loan aligns with your business goals.

Business Loan Interest Rates, Fees, and True Cost

The cost of borrowing for small businesses varies significantly by loan type, lender, and risk profile.

Interest Rates

Traditional bank loans: 5–10%

SBA loans: 6–9%

Online lenders / alternative financing: 8–20%

Merchant cash advances: 20–60% effective APR

Fees

Origination fees: 1–4% of the loan amount

Application fees: $50–$500

Prepayment penalties (sometimes applicable)

Late payment fees

True Cost

Lenders also evaluate risk through fees and APR. Even if the interest rate appears low, hidden costs can increase the effective borrowing cost. Businesses must calculate total repayment including interest, fees, and operational holding costs to determine whether the loan is profitable.

ROI and Financial Impact

Borrowing can amplify growth, but mismanaged loans can quickly erode profits. ROI is calculated by evaluating revenue generated from the loan versus the total cost of borrowing.

Example ROI factors:

Increased sales from expanded operations

Cost savings from bulk inventory purchases

Tax benefits from equipment financing or interest deductions

Proper financial modeling, scenario planning, and conservative assumptions help ensure the borrowed funds contribute positively to the business’s growth trajectory.

Real-World Case Study

Business Profile: Mid-sized retail business Loan Type: SBA 7(a) Loan Loan Amount: $150,000 Purpose: Expand inventory and hire additional staff Term: 7 years, fixed interest rate 7%

Results:

Increased monthly revenue by 30% within six months

Hired 3 additional employees

Loan repayments structured monthly, manageable within cash flow

ROI: $45,000 net profit increase in the first year

This example demonstrates how structured financing, aligned with business goals, can create measurable growth and improve long-term sustainability.

Local Considerations, Lender Selection, Comparisons, FAQs, and Long-Term Strategy

Successfully accessing business loans for small businesses involves more than understanding loan types and rates. Geographic factors, lender relationships, risk assessment, and long-term financing strategy play a critical role in maximizing growth while minimizing costs and financial strain. This final section addresses these advanced considerations.

Small Business Loans Near Me

When searching for “small business loans near me,” geography matters. Lenders’ availability, interest rates, terms, and approval speed vary by city, state, and country. Local banks, credit unions, and community lenders often understand regional market dynamics better than national lenders.

Advantages of local lending:

Faster loan processing and approvals due to proximity

Knowledge of local business conditions and regulations

Personalized support and relationship-based approvals

Access to community-focused programs and grants

For example, small businesses in Texas or Florida may have access to multiple SBA-backed lenders with local expertise, while startups in New York or California may face stricter underwriting and higher costs due to higher operational and regulatory expenses. Entrepreneurs should evaluate the lender’s understanding of local market trends, including commercial real estate values, industry-specific risk, and economic cycles.

Local lenders also provide networking opportunities, often connecting business owners to mentors, regional development programs, and other resources that enhance long-term growth.

How to Choose the Best Lender for Small Business Loans

Selecting the right lender is crucial. The wrong lender can lead to high costs, inflexible repayment terms, and missed growth opportunities. Business owners should consider:

Transparency – Clear disclosure of interest rates, fees, prepayment penalties, and repayment schedules.

Speed – Ability to approve and fund loans quickly, especially in competitive or time-sensitive markets.

Flexibility – Customizable draw schedules, repayment terms, and willingness to work through unforeseen issues.

Reputation and Experience – Track record of supporting small businesses in your industry or region.

Before committing, ask questions such as:

How is interest calculated and compounded?

Are there early repayment or prepayment penalties?

What collateral or personal guarantees are required?

How quickly can funds be disbursed once approved?

Building a strong lender relationship can provide long-term benefits, including access to higher loan amounts, better rates, and flexible terms as your business grows.

Business Loans vs Alternative Financing

While traditional business loans are widely used, alternative financing options like merchant cash advances, invoice factoring, and online loans provide additional flexibility. Comparing options is critical to ensure the cost of borrowing aligns with cash flow and business goals.

Feature

Traditional Loans

Alternative Financing

Interest

Lower

Higher (often 20–60% APR)

Approval Speed

Moderate

Fast (days)

Risk

Moderate

High

Documentation

Extensive

Minimal

Businesses with predictable cash flows often benefit most from traditional loans, whereas businesses requiring immediate access to capital or with limited documentation may use alternative financing, keeping in mind the higher cost and risk.

Business Loans FAQs

Q1: Can startups qualify for small business loans? Yes. While startups face stricter scrutiny, SBA microloans, online lenders, and private lending options allow eligible startups to access capital.

Q2: How much can a small business borrow? Loan amounts vary widely, from $5,000 microloans to $500,000+ SBA term loans, depending on creditworthiness, business size, and lender policies.

Q3: How fast are business loans approved? Traditional banks: 2–6 weeks, SBA loans: several weeks to months, online lenders: 1–7 days.

Q4: Are business loans risky? Loans carry risk if cash flow is insufficient. Proper planning, conservative borrowing, and repayment discipline reduce risk significantly.

Q5: Can business loans be used for any purpose? Most lenders restrict the use of funds to business-related expenses. Terms and allowable uses should always be confirmed.

Long-Term Small Business Financing Strategy

Accessing capital strategically allows businesses to scale responsibly and sustainably. Long-term strategies include:

Recycling Capital – Using loan proceeds for growth and reinvesting profits to reduce reliance on debt.

Building Credit – Timely repayment of loans strengthens business credit, unlocking better future financing.

Diversifying Financing Sources – Combining SBA loans, term loans, lines of credit, and private funding reduces dependency on a single lender.

Aligning Loans with Business Goals – Matching loan types and repayment structures to operational and expansion objectives minimizes financial strain.

The most successful small businesses treat borrowing as a growth tool rather than a short-term fix, ensuring that loans generate more value than they cost.

Final Verdict: Are Business Loans for Small Businesses Worth It?

Business loans for small businesses are a powerful tool for growth, expansion, and operational stability. When chosen wisely, with careful attention to lender selection, repayment planning, and cash flow management, these loans can accelerate revenue growth, create jobs, and enable long-term sustainability.

However, borrowing without planning or understanding loan terms can lead to financial stress, high costs, and reduced profitability. Successful borrowers focus on strategic alignment, conservative assumptions, and long-term relationships with reputable lenders.

For small business owners seeking capital without giving up equity, structured financing through the right loan can be both safe and highly effective. With disciplined management, business loans are not just a funding option—they are a strategic growth lever.